Buy-Sell Agreements

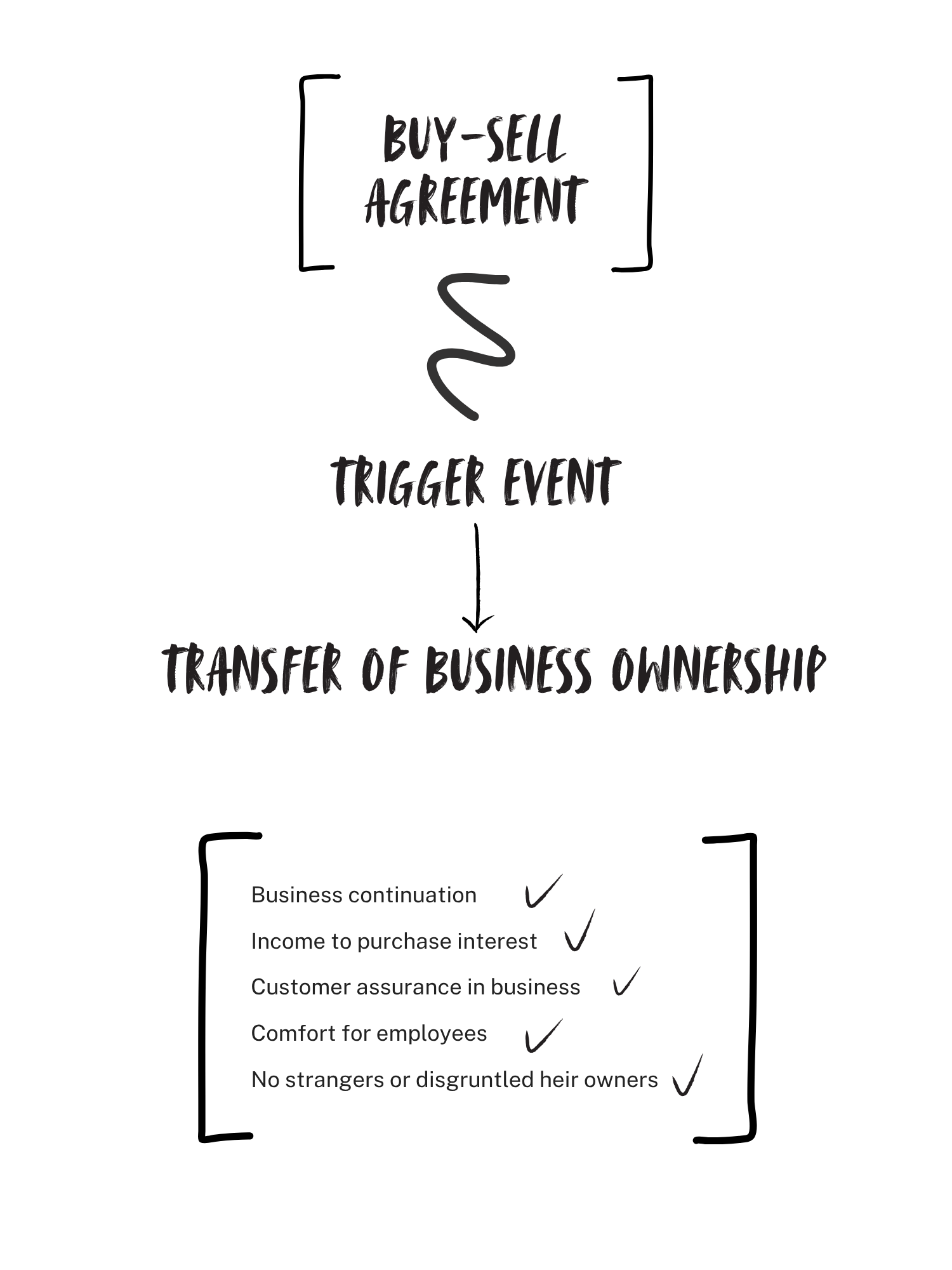

A buy-sell agreement ensures stability in business transition and prevents heirs from having to run or sell the business after an owner dies. With a buyer in place, a life insurance policy ensures that funds will be available when needed.

How It Works:

There are three main types of buy-sell agreements:

Cross-purchase agreement

Each owner buys part of the interest. Each owner buys insurance on every other owner to fund the purchase.

Entity-purchase agreement

The business itself buys the interest. The business buys insurance on each owner to fund the purchase. Some entity-purchase agreements might have undesirable tax consequences.

One-way agreement

An individual (usually a key employee) agrees to buy a sole-owner business. The buyer typically purchases life insurance on the owner to fund the purchase.

Why Is It Useful?

A buy-sell agreement ensures an orderly transition and alleviates conflicts over the value of a business. Heirs get needed cash, and surviving owners are assured that the heirs or a stranger cannot insert themselves into the business.

Funding the Agreement

Without proper funding, even the best‑written agreement is not a solution. Options for funding the agreement include cash reserves, borrowing funds, installment payments to heirs, liquidation of assets or investments, disability buy-out insurance, life insurance or a combination of funding methods. Life insurance is the most common funding method for buy-sell agreements because it provides immediate liquidity at exactly the moment it’s needed. But owners should also review:

- Whether the policy amount still reflects the current business value

- Whether disability buy‑out coverage is needed (often overlooked)

- Whether the business or the owners should own the policy for tax efficiency

- Whether term or permanent insurance is more appropriate for the long‑term plan

What Most Business Owners Overlook

A buy-sell agreement only works if it's properly valued and properly funded. Many owners draft an agreement once and never revisit it, even as the business grows, partners change, or tax laws shift. An outdated valuation formula or underfunded insurance policy can leave surviving partners scrambling for cash, or force heirs to accept far less than the business is worth.

When to Update Your Buy-Sell Agreement

A buy‑sell agreement should be reviewed every few years or when major events occur, such as:

- Adding or removing partners

- Significant revenue growth

- Taking on debt or investors

- Changes in tax law

- Succession planning updates

These reviews ensure the agreement still reflects the business’s true value and the owners’ intentions.

SUMMARY:

A buy-sell agreement is a legally binding contract - whether simple or complex - that dictates the terms of a future sale of a business interest, ensuring continuity of ownership and management. It specifies the triggering circumstances (retirement, death, disability), the buyer(s), and how the business will be valued.

This information is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor.

Copyright © 2026, PGI Partners, Inc., 921 East 86th Street, Suite 100, Indianapolis, Indiana 46240. All rights reserved.

This material was prepared by PGI Partners, Inc. on behalf of LPL Financial, LLC.